Salary sacrifice: Will it still be worth it in 2029?

The Chancellor's announcement that NI-exempt salary sacrifice pension contributions will be capped at £2,000 a year from April 2029 has, understandably, been received with alarm.

On the surface, this change might look like it will drastically diminish the commercial value of one of the main tools employers have to help both themselves and their employees save money, just as the average wage is going up. But I think it's important to look at the bigger picture.

Yes, NI savings will reduce when the new rules kick in. But salary sacrifice is still very much worth doing. If anything, now is the time to double down, not pull back.

What's changing from April 2029?

The key change to pension salary sacrifice schemes from April 2029 relates to NI. It does not impact income tax, or how much of their salary an employee can sacrifice.

The first £2,000 contributions sacrificed each year will be NI-exempt, while contributions over that threshold will attract NI at the usual rates. The NI saving will reduce. But the scheme will continue to achieve the same outcome it achieves today: a reduced NI bill for both the employer and employees.

For employees on average pay there will be very little change, if any. For higher earners, a well-designed salary sacrifice scheme will keep reducing taxable income and income tax liability.

The latter point is particularly important because, with personal tax thresholds frozen until 2028, a growing number of employees who wouldn't usually hit the 'higher earner' bracket are being pushed into higher-earner tax territory.

The impact of the April 2029 changes: a worked example

So, how will introducing a cap on NI-exempt salary sacrifice pension contributions change the financial picture for the average employee?

In reality, far less than you'd think.

Let's say an employee earns £60,000 a year. Frozen tax thresholds and the ensuing fiscal drag means they'll pay higher-rate tax on more of their earnings, increasing their total tax bill to £11,432.

Under current rules, sacrificing £5,000 of their salary and paying into the pension would result in a £2,100 combined tax and NI saving.

Under 2029 rules, the £2,000 income tax savings would stay the same. What will change is that NI will still be due on £3,000 of the contribution. That means an extra £60 in NICs – it's still a big saving, overall.

It's a trap: the 60% effective tax rate for higher earners

One of the misleading myths around the 2029 changes is that salary sacrifice will no longer help those earning £100,000 a year and above. But, here again, the reality is that salary sacrifice will continue working just as well, even when you factor in the reduced NI savings.

The key reason for this is the tapering of the personal allowance above £100,000, which means higher earners can end up paying tax at an effective marginal rate of 60%. Salary sacrifice contributions counteract this, even after 2029.

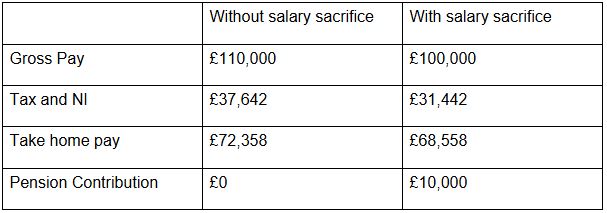

Say an employee earns £110,000 a year. At this level, the tax-free personal allowance is tapered to £7,570, so their total taxable income is £102,430.

That works out at around £33,432 in tax. Sacrificing £10,000 restores the full personal allowance, reducing the employee's tax bill to £27,432 and putting £10,000 into their pension.

In this example, the employee is getting the benefit of an extra £6,200, albeit in their pension pot.

From April 2029, the employee will retain that saving but pay 2% NI on £8,000, which works out at £160. Again, a drop in the ocean compared to the tax bill if salary sacrifice weren't an option.

Fiscal drag is a ticking time-bomb but salary sacrifice will defuse it past April 2029

Let's face it. The realisation that a pay rise, bonus, or promotion – even a significant one – won't make much difference to an employee's take-home pay often comes as an unpleasant (and hard to fathom) surprise.

Over time, it's a recipe for disillusionment and disengagement. Employees will rightly question whether extra pay is worth it.

The good news is that the numbers don't lie. With the £2,000 NI exemption cap or not, pension salary sacrifice schemes will remain as valuable as ever. But it's up to employers to make this crystal clear.

Proactively educating employees and building salary sacrifice into pay, promotion, and bonus conversations will help them benefit more from their salary … and help employers unlock more value from a benefit they're already funding.

Is your workplace pension a win-win for your business and employees? Score your scheme, benchmark against other UK employers, and get tips for better outcomes by downloading your Cushon scorecard here.

Supplied by REBA Associate Member, Cushon

Cushon is a workplace pensions and savings provider with an award-winning proposition.