Why internationally mobile employees need an international retirement solution

With the traditional expatriate model under pressure due to cost, multinationals still need to respond to increasing international staff mobility and send people overseas to support their business. Benefits remain high on the agenda of these mobile employees and retirement savings must still be met by the employer, whether this is driven by employment contracts, a global benefits strategy or recruitment and retention issues.

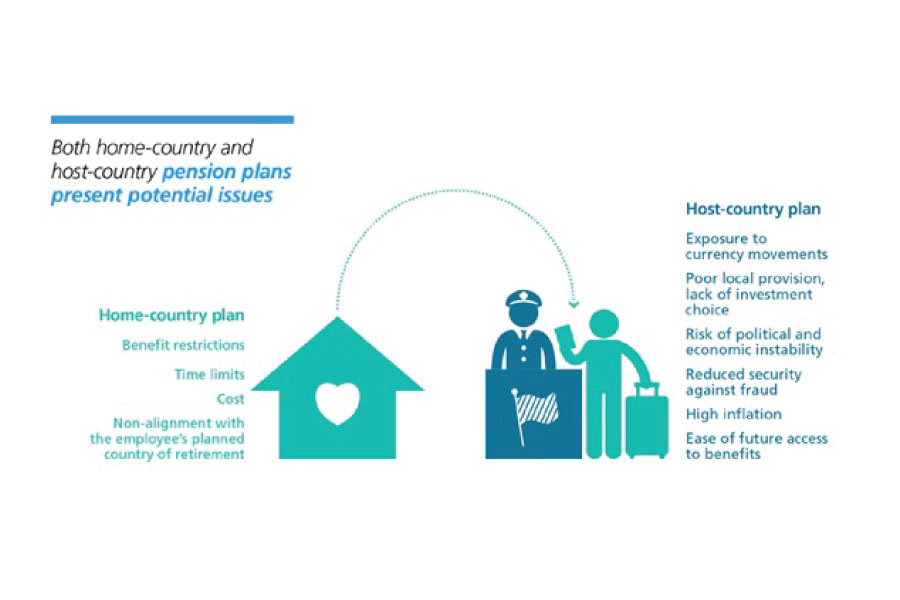

Local pension solutions are often not the answer due to low contribution limits and investment restrictions. In addition, building up a pension in countries other than where you intend to retire, perhaps in a weak currency, is simply not attractive.

Solutions

Solutions

What if there were a solution to help the HR function with the challenge of providing good quality pension benefits for overseas assignees? What features would it have?

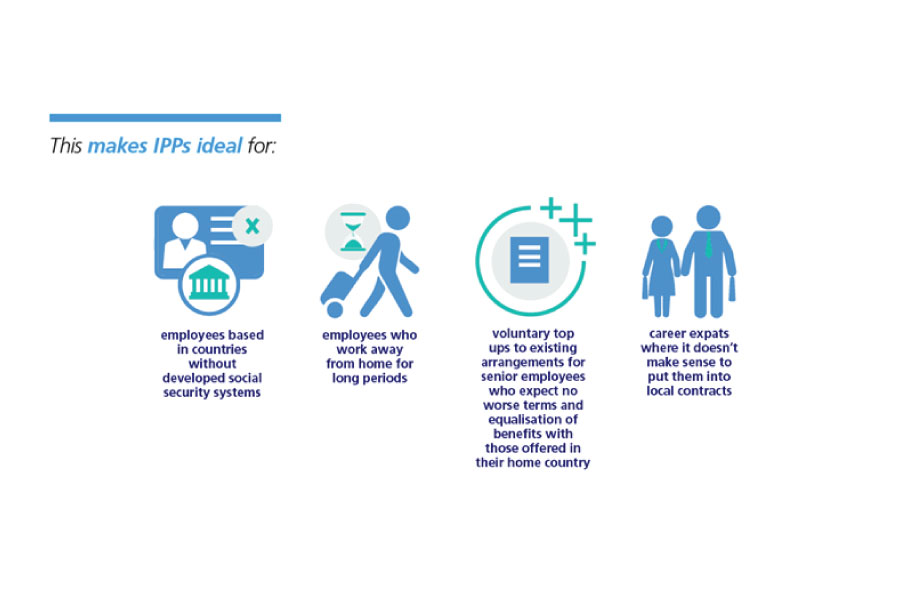

It would allow membership of multiple nationalities, living and working in multiple countries. Contributions would be in any currency and investment could be made into a world-wide range of investment funds. Growth would be tax-free and the entire proceeds could be withdrawn as a tax-free lump sum on retirement or withdrawn as a regular income, again in any currency. Perhaps up to 50 per cent of the fund could be drawn down earlier, to pay off a mortgage, for school fees or whatever the individual wishes. There would be no limits on what the employer or the employee could contribute to the plan and no lifetime allowance restrictions. Payments in would also avoid local social security charges and proceeds would avoid any form of inheritance tax. The only restriction would be that employers could build in vesting scales to enable them to use the plan as a recruitment and retention tool – so, for example, the employee would only become entitled to the company’s contributions after five years of continuous service.

IPP

Does this sound too good to be true? Well, in fact it already largely exists in the form of an international pension plan (IPP).

IPPs are a simple, low-cost savings solution designed for long-term savings and retirement planning. They avoid the problem faced by mobile employees of having multiple pension pots in several countries, all with different social and labour laws, restrictions on contributions, limited investment options and the risk of local currency movements.

In our next articles we’ll be looking at how giving employees the right investment options can make an IPP even more attractive.

In our next articles we’ll be looking at how giving employees the right investment options can make an IPP even more attractive.

In the meantime, here’s an overview of the Zurich International Pension Plan to highlight how an IPP can adapt to fit the specific needs of your organization:

This article is sponsored by Zurich.

This article is sponsored by Zurich.

Supplied by REBA Associate Member, Zurich

At Zurich, we’re proud to have been providing UK insurance for over 100 years. Whatever you’re looking to support or protect, we’ll do our best to help you.